Why Are Brits Still So Obsessed with Cash?

Why Holding Too Much Cash Might Be Holding You Back

This week, we're cutting through the noise to bring you the insights you need to navigate the landscape of financial markets, planning and investments. Here’s what we will be covering today:

Why High Earners Are Feeling the Squeeze — Even Without a Mortgage

Earning Over £100k? Why Your Tax Bill Feels Higher Than Ever

Is Property Investment Still “Safe as Houses”?

Grab a coffee and dive in! 👇

Personal Insight

Did you know that only 8% of the UK’s household financial assets are held in stocks? That’s the lowest across the G7. Compare that to Sweden, where it’s closer to 70%.

It’s no wonder the UK economy feels sluggish — too much of our money is sitting idle, earning next to nothing after inflation, rather than being put to work in the markets.

Why is this?

For many people I speak to, it’s psychological, not logical.

Fear of Loss: “I don’t want to lose money” is the most common reason. The headlines love a good stock market crash story, but rarely report on the quiet, compounding effect of markets over time.

Past Trauma: Some still carry scars from 2008 or more recently 2020.

Comfort in Certainty: Cash feels safe. You can see it. Touch it. It doesn’t fluctuate. But that perceived “safety” comes at a hidden cost: erosion by inflation.

In reality, the bigger long-term risk is not volatility — it’s stagnation.

If you’re sitting on cash, ask yourself:

Is this money for the short-term? (If yes, cash is fine.)

Is this money for the long-term? (If yes, doing nothing may be costing you far more than you realise.)

What can you do?

Start small. Build confidence over time. Understand that investing isn’t gambling — it’s owning a piece of businesses, innovation and progress.

Don’t let fear stop your future self from living a wealthier life.

💬 Are you letting fear of risk stop your money from working harder for you? Let me know by sending me a message here. I’d love to hear it and cheer you on! 😊

Latest Market Moves

US equity markets have remained buoyant, with the NASDAQ Composite hitting new all-time highs, driven largely by strong performance from technology stocks. Nvidia, in particular, has become the first company to surpass a $4 trillion market capitalisation, highlighting the dominance of AI and tech in current investor sentiment. This marks an extraordinary milestone considering Apple only reached the $1 trillion mark in 2018.

The S&P 500 has similarly benefited from strength in tech and industrial sectors. Defensive sectors like healthcare and consumer staples continue to lag, with stock-specific weakness in firms such as UnitedHealth and Novo Nordisk.

In the UK, FTSE 100 reached new highs last week, helped by a rebound in mining stocks like Glencore, BHP, and Rio Tinto, as copper prices spiked following Donald Trump's announcement of a 50% copper import tariff set to begin on August 1st. This divergence in copper pricing between the US and UK has lifted sentiment in UK-listed miners, despite broader concerns about slowing global growth.

Macroeconomic Update

UK economic data disappointed, with GDP contracting by 0.1% in May, following a 0.3% decline in April. The OBR's latest report highlighted structural weaknesses in the UK economy: high debt levels, excessive spending and vulnerability to external shocks. This puts increased focus on the upcoming Autumn Budget, where fiscal credibility will be tested.

Policy & Regulation

In domestic savings news, the government has backtracked on proposed cuts to Cash ISA allowances after significant pushback from the financial industry. However, discussions continue around the broader purpose of ISAs and whether they should encourage investment rather than sheltering cash. Historically, the UK has lagged behind peers like Sweden in household equity ownership, with only 8% of financial assets held in stocks compared to Sweden’s 70%.

Rachel Reeves' initiative reflects a long-term ambition to shift savings culture towards productive investment rather than cash hoarding, a potential move to support capital markets and reduce reliance on public debt issuance.

Looking Ahead

This week will see earnings updates from Rio Tinto, BHP, and Netflix, which could provide further direction for markets, particularly in mining and tech sectors.

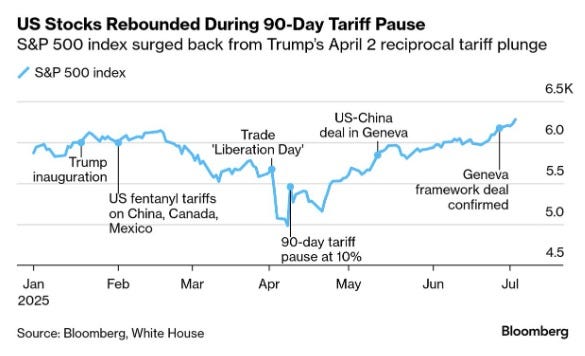

Risk Warning: The performance of your investments is subject to risk(s). This is for informational purposes and does not constitute financial advice, which should be based on your individual circumstances. Full disclaimer below.Chart of the Week

Why High Earners Are Feeling the Squeeze — Even Without a Mortgage.

Once upon a time, earning a six-figure salary symbolised financial freedom, confidence, and a comfortable lifestyle.

But today? Many professionals earning over £100,000 are asking the same question:

"Why doesn’t it feel like I’m doing better than this?"

You're not imagining it. The financial headwinds facing high earners have quietly intensified, leaving many feeling frustrated, taxed to the hilt and underwhelmed by their take-home pay.

Why High Earners Feel the Squeeze More Than Ever

Tuition fees, tax traps, frozen thresholds and inflation are all conspiring against those who should, by right, feel financially secure.

The Legacy of Tuition Fees

Since 2012, university tuition fees have more than tripled to £9,535 per year, with maintenance loans of up to £13,762 annually.

Many graduates today start their careers with £70,000+ in debt (even more for postgraduates).

For high earners, the repayment sting is sharp:

9% of income above £27,295 on undergraduate debt

6% extra for postgraduate loans

No relief for rising salaries: the repayment threshold has been frozen since 2021

If you earn £100,000+, you could easily be repaying over £10,900 per year towards student loans alone.

Unlike average graduates, you’ll pay it off faster — but it means your disposable income feels permanently squeezed.

The 60% Tax Trap

On top of loan repayments, many high earners fall foul of the stealthiest tax trap in Britain.

Once your income exceeds £100,000, you begin losing your personal allowance (£12,570) — £1 lost for every £2 earned over the threshold.

The result?

Earn £10k more and potentially keep only £4k after tax.

(A more detailed insight into this is below)

Frozen Allowances, Rising Costs

The personal allowance has been frozen since 2021.

The higher-rate threshold is also frozen.

Inflation has driven costs up dramatically, but the tax thresholds have not moved.

National Insurance and student loan repayments further erode take-home pay.

£125,000 in 2020 isn’t worth £125,000 in 2025.

In fact, to achieve the same real-terms disposable income as someone earning £125,000 four years ago, you'd now need to earn closer to £210,000.

Why Smart Planning Is Now Essential

Many clients in this position tell me:

“I thought six figures would change my life, but I don’t feel any wealthier.”

That’s because salary alone is no longer a good measure of financial wellbeing.

Today, what you keep and how you grow it matters far more than what you earn.

How I Help Clients Solve This Problem:

✅ Tax Planning: Structuring income, pensions, and investments to legally reduce exposure to higher rates.

✅ Debt Strategy: Reviewing loan repayment timing, interest rates and allowances to accelerate freedom from student debt.

✅ Investment Planning: Using ISAs, pensions and diversified portfolios to build wealth tax-efficiently.

✅ Retirement Planning: Ensuring today’s income decisions protect tomorrow’s lifestyle.

✅ Cashflow Forecasting: Showing clearly how today’s decisions shape your financial future.

If you’re earning six figures but wondering why it doesn’t feel like you’re winning, you are not alone. But you don’t have to accept it.

Risk Warning: Taxation legislation may change in the future. Tax treatment is based on individual's unique circumstances. The performance of your investments is subject to risk(s). This is for informational purposes and does not constitute financial advice, which should be based on your individual circumstances. Full disclaimer below.

Earning Over £100k? Why Your Tax Bill Feels Higher Than Ever

More people than ever are earning six-figure salaries. Last year alone, 1.35 million people in the UK earned over £100,000. At first glance, that sounds like financial success. But for many, the reality feels very different. Why?

Because earning over £100k in Britain today often means walking straight into one of the most punishing and misunderstood tax traps in our system.

Welcome to the ‘60% Tax Trap’.

How the Trap Works (And Why It Matters to You)

Once your income passes £100,000, you begin to lose your tax-free personal allowance (£12,570).

For every £2 earned over £100k, you lose £1 of allowance.

By the time you reach £125,140, you have no personal allowance left.

The effective result?

The income you earn between £100,000 and £125,140 is taxed at an eye-watering 60%.

Not through a ‘special’ tax rate, but because of how allowances are clawed back alongside standard tax bands.

Why £100k Doesn’t Feel Like £100k Anymore:

Inflation: £100,000 today is worth about £81,000 in 2021 money.

Frozen thresholds: Personal allowance has been frozen despite rising incomes — a stealth tax by design.

Erosion of real-term income: Higher earners are taking home less than they expect.

Who’s Affected?

50% of people earning £100k+ now fall into this trap.

Fastest-growing groups: Professionals in North East England.

Largest concentration: London and South East.

Why It’s Not Hopeless — Smart Planning Can Fix This.

Just because you’re in this trap doesn’t mean you’re stuck.

With the right financial strategy, you can:

✅ Reclaim lost allowances.

Through pension contributions, you can reduce your ‘net’ income below the threshold and effectively recover your personal allowance.

✅ Minimise unnecessary tax.

Using allowances, ISAs, and tax-efficient investment vehicles helps shelter future growth.

✅ Optimise your long-term position.

Pensions, trusts and family wealth structures allow you to redirect money more tax-efficiently.

If You’re Earning £100k+ — Planning Matters More Than Ever.

Don't let poor tax planning erode your hard-earned income. The £100k milestone should be a cause for celebration — not frustration.

Together, we can review:

How exposed you are to the 60% trap

How to make your earnings work harder

How to build wealth more tax-efficiently

Take back control. Pay less tax. Build more wealth.

Risk Warning: This is for informational purposes and does not constitute financial advice, which should be based on your individual circumstances. Full disclaimer below.

Is Property Investment Still “Safe as Houses”?

Why the ‘golden era’ could be behind us — and what smart investors should focus on now.

For decades, property has been the cornerstone of wealth building in the UK. But today’s environment looks very different from the past — and relying on house price growth alone is no longer the sure thing it once was.

What’s changed?

Recent research from Rathbones highlights that, since 2016, residential property growth has barely kept pace with inflation — just 3.7% per annum on average across the UK. London, historically a hotbed for property gains, has underperformed even further.

Compare this with global stock markets:

£100 in UK property since 2016 → worth £134 today

£100 in a diversified global equity portfolio → worth £174 today

Why has this shift happened?

🔸 Interest rates aren’t falling like they did in the 80s-2000s

🔸 Government policy is less friendly to landlords (tax, regulation)

🔸 Higher property prices are stretching affordability

🔸 Rental yields are stagnating in many areas

Does this mean property is ‘dead’?

Not at all — but the easy money days are gone. Success in property now relies on adding value through:

✅ Development

✅ Specialist niches (HMOs, supported housing)

✅ Focusing on income, not capital growth

Meanwhile, diversified global investments offer greater flexibility, liquidity and often stronger long-term returns.

So, where should you focus?

✔ Your home is still a foundation of financial security — repaying your mortgage reduces future living costs and provides stability.

✔ Investment properties need careful scrutiny — look beyond headline growth to rental yield, tax efficiency and long-term viability.

✔ Stock markets remain a powerful tool for building real, liquid wealth, especially when used alongside pensions and ISAs.

It’s not about choosing property vs. stocks. It’s about building a balanced, resilient plan that serves your long-term goals — with the right mix of property, investments and tax-efficient structures.

Risk Warning: This is for informational purposes and does not constitute financial advice, which should be based on your individual circumstances. Full disclaimer below.📞 Contact us today to review your wealth strategy and see how prepared you are for the long haul!

Top Trending News In Finance

Here are the 3 most important financial news, you need to know about!

#➌ Trump Threatens 30% Tariffs on EU & Mexico. President Trump has escalated the US trade war by proposing a 30% tariff on imports from the EU and Mexico, set to take effect August 1 unless a deal is reached. This move deepens economic tensions and could provoke retaliation from key trade partners

#➋ Fed’s Christopher Waller Pushes for July Rate Cut. Federal Reserve Governor Christopher Waller is among a minority advocating for a rate reduction in July 2025, arguing that the current monetary policy is overly restrictive despite strong job data and cooling inflation. He’s also proposing shifts toward short-term Treasuries to manage balance-sheet risk

#➊ RBC Raises S&P 500 Year-End Target to 6,250. RBC Capital Markets has increased its year-end forecast for the S&P 500 from 5,730 to 6,250, citing improving investor sentiment and optimism about 2026 earnings growth. This reflects strong institutional confidence in the US equity market

Thanks for staying connected and being part of the Fast Financier’s Inner Circle! I look forward to sharing more insights with you next time. Until then, keep striving toward your goals and remember—Feel free to hit reply if you need any guidance or have questions. You can also chat with us on WhatsApp here 💬. Wishing you continued success on your financial journey!

Kind regards,

Gavin Pannu

Tradenomic Financial

0203 376 0575

gavin@tradenomic.co.uk

LinkedIn | Website | Book Discovery Call

An important Risk Warning:

Your home may be repossessed if you do not keep up repayments on your mortgage. Levels and bases of, and reliefs from taxation are subject to change and their value will depend upon personal circumstances. Taxation and pension legislation may change in the future. Tax treatment is based on individual's unique circumstances. The Financial Conduct Authority (FCA) does not regulate Wills, Inheritance Tax Planning or Trust advice.

The performance of your investments is subject to risk(s). Its performance may fluctuate based on movements in the market and economic condition(s). Capital at risk. Currency movements may also affect the value of investments. The value of an investment may fall as well as rise. You may get back less than you originally invested. Past performance is not a reliable indicator of the future performance.

Tradenomic Financial is the trading name of Tradenomic Limited which is an Appointed Representative of Julian Harris Financial Consultants, authorised and regulated by the Financial Conduct Authority No. 994930.

As a regulated professional, I aim to be straightforward and provide tools to help you on your journey to financial freedom. Please note, all content shared here is for educational purposes only and not to be seen as specific financial advice. I don’t know your unique circumstances, so general insights may not apply to you. The views expressed are my own.

While we use reliable sources and take care in compiling information, all data and opinions are subject to change without notice. This content is not a recommendation or solicitation to buy or sell securities. Investments carry risk, so please conduct your own research and consult an authorised adviser. This newsletter and any correspondence email is for informational purposes and does not constitute financial advice, which should be based on your individual circumstances. The content within contains our observations of current trends and does not constitute a personal recommendation.

Additional Resources:

🔗 Curious about your financial standing? Use our Net Worth Calculator to find out where you stand today!

🔗 Visualise the trends! Explore our Financial Markets Chart Gallery to stay ahead of the curve.

🔗 Check your credit score now and gain valuable insights to help you stay on top of your financial health. Try it FREE for 30 days, then £14.99 a month - cancel online any time.

Life’s Big Questions to Ask Yourself: