War, Uncertainty & the Markets

What history teaches us about war, fear and staying invested.

You may have noticed a short break in your weekly newsletter—over the past two weeks, I’ve been deep in research and discussions around emerging investment opportunities that could shape the next six months. Sometimes, stepping back allows me to bring more meaningful insights… and I’m excited to bring this to you.

This week, we're cutting through the noise to bring you the insights you need to navigate the landscape of financial markets, planning and investments. Here’s what we will be covering today:

Freedom by starting a Pension in Your 20s

The Estate Documents Everyone Needs

The Thinking Skill That Could Save You Thousands

Grab a coffee and dive in! 👇

Personal Insight

With headlines once again filled with geopolitical tensions—this time focused on the Middle East—it’s natural to feel anxious about what lies ahead. I’ve been reflecting on how deeply interconnected global conflict and our personal finances really are.

History tells us that markets hate uncertainty. And few things are more uncertain—or unsettling—than the risk of war.

But here’s something less commonly known: the immediate reaction in financial markets isn’t always what people expect. Yes, there’s often a sharp emotional response—stocks can drop, oil prices can spike and safe havens like gold or the US dollar may rally. But over the medium to long term, markets have a remarkable ability to adapt, absorb and even recover.

For example, during the early stages of the Iraq War in 2003, the markets dipped—but within months, they had rebounded strongly. The same pattern repeated during other conflicts, like the Gulf War or even the Cuban Missile Crisis. Fear drives volatility—but resilience drives recovery.

That doesn’t mean we ignore the risks. On the contrary, it’s a reminder to respect the risks without reacting impulsively.

If you find yourself wondering, “Should I sell now before things get worse?”—pause. Ask yourself: Am I investing for the next six days... or the next six years?

Staying informed is important. But staying disciplined is what protects your wealth.

If you’re feeling uneasy about what’s happening globally and how it might affect your financial future, I’m here to help you navigate it calmly and with clarity.

💬 When headlines turn frightening, do you find yourself tempted to make changes to your investments—or do you stay the course? Let me know by sending me a message here. I’d love to hear it and cheer you on! 😊

Latest Market Moves

Bank of England Holds Steady Amid Inflation Concerns

The Bank of England (BoE) held interest rates at 4.25% as expected, with a 6-3 split among policymakers. Governor Andrew Bailey reiterated that rates are on a "gradual downward path," though the BoE remains cautious, citing persistent inflation and global uncertainty. UK inflation eased slightly in May to 3.4%, with services inflation—closely watched by the BoE—falling to 4.7%, in line with forecasts.

Federal Reserve Keeps Rates Unchanged, Eyes Potential Cuts

As anticipated, the Federal Reserve held its target rate steady at 4.25%–4.5% for the fourth consecutive meeting. Chair Jerome Powell acknowledged elevated uncertainty but described the economy as "solid." The Fed’s updated projections still point to two rate cuts this year, though inflation and unemployment expectations for 2025 ticked higher and GDP forecasts were revised down. Fed Governor Waller hinted that a July rate cut is possible, giving markets a late-week lift.

US Economic Data Mixed

Economic indicators painted a cloudy picture:

Retail Sales fell 0.9% in May (second monthly drop), though core sales rose 0.4%.

Homebuilder Sentiment dipped, with the NAHB Housing Market Index falling to 32—its lowest since December 2022.

Housing Starts dropped nearly 10% in May to the weakest pace since May 2020.

Geopolitical Tensions Weigh on Sentiment

Markets turned cautious as Middle East tensions flared. US strikes on Iranian nuclear sites raised fears of retaliation and energy disruption. Brent crude spiked to $78 a barrel before easing, but analysts warn of a potential surge toward $100–$110 if the Strait of Hormuz is impacted. European and US equity futures softened, while Treasury yields rose and the dollar strengthened slightly.

Looking Ahead

Markets are on alert for any escalation from Iran and will closely watch Fed Chair Powell’s upcoming remarks for clues on the timing of potential rate cuts—especially as energy-linked inflation risks begin to resurface.

Feel free to reach out if you’d like to chat about how to position your investments for success — I’m here to help you make sense of it all.

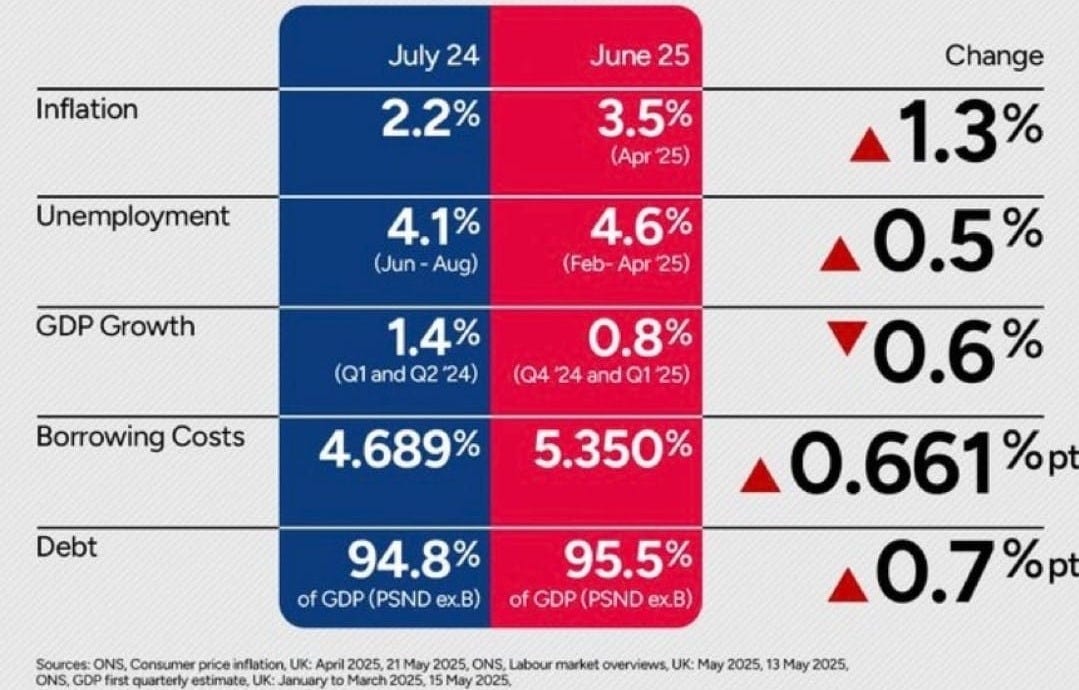

Risk Warning: The performance of your investments is subject to risk(s). This is for informational purposes and does not constitute financial advice, which should be based on your individual circumstances. Full disclaimer below.Charts of the Week

Pensions in Your 20s: The Secret to Buying Freedom Later

£800,000—The New Retirement Wake-Up Call

Imagine being told that you might need up to £800,000 to retire comfortably. Sounds extreme? It’s not. That’s the latest figure from the Pensions and Lifetime Savings Association (PLSA)—and with inflation on the rise, this number could grow.

If you’re in your 20s, this is exactly the moment you need to act. Your choices now will shape your options decades from today—when you’ll be relying on your past self to fund your future freedom.

Why Your 20s Are Your Financial Power Years

Freedom vs. Foundations

At 20-something, you’re enjoying your first taste of financial independence—holidays, nights out, perhaps your first full-time job. Saving for retirement may feel like worrying about grey hair before it grows. But here’s the truth: your 20s are your greatest opportunity.

“Your 20s are really when you need to do the most work on your savings.”

It’s not about locking yourself away from enjoyment. It’s about making smarter choices early so that you can live with more freedom later.

Build a Financial Safety Net First

Before investing for the long term, I recommend building a cash cushion—six month’s salary in an easy-access savings account—to protect yourself from life’s curveballs, like job loss or emergencies.

Once you’ve built that safety net, it’s time to focus on your retirement savings.

Why Early Pension Saving Pays Off—Literally

Let Your Employer Boost Your Future

Most 20-somethings are eligible for a workplace pension, and many employers will match your contributions, often up to 8%. That’s free money—and walking away from it is like declining a pay raise.

Don’t be tempted to opt out just to boost your monthly paycheck. What seems like a short-term gain is actually a massive long-term loss.

The Magic of Compound Growth

If you put just £100 per month into a pension growing at an average of 7% annually, over 45 years you could build a pot of nearly £380,000. That’s halfway to the PLSA’s comfortable retirement target, from just the cost of a weekly takeaway.

And since the money comes directly out of your paycheck, you’ll barely notice it’s gone—until you’re older and very grateful you started.

Start Now, Save Smart, Live Free Later

Automate Contributions

The simplest way to get started? Automate a monthly amount into your pension. Think of it as paying your “future self” first.

Starting Late Costs More

If you wait until age 40 to start saving, you may need to contribute four to five times as much each month to reach the same pot—just to catch up. Many people simply can’t afford that, meaning their retirement goals are compromised or delayed.

“For many people, a comfortable retirement is not achievable if you start late.”

Buy Future Flexibility

Early savers buy more than just security—they buy freedom. The freedom to switch careers, raise a family, take time off, or retire early. Late starters are often locked into higher-paying but less fulfilling jobs just to fund retirement.

A well-funded pension in your 50s or 60s is not just a number. It’s control over your life.

A Pension Isn’t for When You’re Old—It’s for When You Want Options

It’s easy to dismiss pensions as something for your future self to worry about. But your future self is depending on you now.

By automating small contributions, using your workplace pension and allowing time to work its compounding magic, you’re setting the foundation for financial freedom, flexibility and peace of mind.

Remember: a pension is just a pot of money you'll use later. The earlier you fill it, the more freedom you'll enjoy when you need it most.

Start small. Start early. Start now.

Your future self will thank you.

Risk Warning: Taxation legislation may change in the future. Tax treatment is based on individual's unique circumstances. The performance of your investments is subject to risk(s). This is for informational purposes and does not constitute financial advice, which should be based on your individual circumstances. Full disclaimer below.

The Estate Documents Everyone Needs

Estate Planning Isn’t Just for the Wealthy or Elderly

What would happen to your finances if you were suddenly incapacitated—or worse?

Too many people assume estate planning is something to worry about “later.” But if you don’t have a plan, the law decides for you—and that can be expensive, stressful and messy for your family.

Proper estate planning ensures your loved ones are protected and your wishes are respected. It’s not just about wills—it’s about creating a safety net for life’s most unpredictable moments.

The Core Documents That Protect You and Your Family

1. Financial Power of Attorney

This document allows someone you trust (your “agent”) to manage your finances if you’re unable to. They can pay your bills, access accounts or apply for benefits on your behalf.

✅ Pro: Crucial for maintaining continuity in your financial affairs if you're incapacitated.

⚠️ Con: Must be drafted with care—an overly broad power of attorney can be misused if given to the wrong person.

2. Health Care Power of Attorney & Living Will

A health care power of attorney lets someone make medical decisions for you. A living will (aka advance directive) records your end-of-life care wishes.

✅ Pro: Removes guesswork and emotional burden from your family during medical crises.

⚠️ Con: If not updated or discussed clearly, loved ones may still feel uncertain or conflicted.

3. A Will

Your will directs how your individual assets should be distributed and who should care for minor children.

✅ Pro: Ensures your wishes are followed and gives you control over guardianship decisions.

⚠️ Con: Wills must go through probate, which can be slow and costly depending on the state.

4. Revocable Trust

This flexible tool helps manage and distribute assets while avoiding probate. It also ensures a smooth transition if you become incapacitated.

✅ Pro: Provides privacy, speed and flexibility.

⚠️ Con: More complex and expensive to set up than a will alone—may not be necessary for smaller estates.

5. Beneficiary Designations

These apply to life insurance and retirement accounts, bypassing wills or trusts entirely. Ensure they're current—outdated forms override your will.

✅ Pro: Fast, efficient asset transfer without legal delay.

⚠️ Con: If neglected, these designations can accidentally leave money to the wrong person.

Why You Need a Trusted Team and Regular Reviews

Even the best-drafted documents fail if no one is prepared to carry them out.

You’ll need to name:

An executor for your will

Trustees for any trusts

Agents under your powers of attorney

These people act as fiduciaries—handling everything from asset distribution to tax filings. The right choices bring peace of mind; the wrong ones can create legal and emotional chaos.

✅ Pro: You can empower responsible people or professionals to handle your legacy.

⚠️ Con: If your choices lack financial savvy—or simply aren’t willing—the process can stall or go sideways.

Also, don’t treat your estate plan as “one and done.”

Life changes—so should your documents. Marriage, divorce, births, deaths, moves, or major financial shifts all call for updates.

Start Now, Not Someday

Whether you’re 28 or 68, estate planning is about taking control—not leaving things to chance or the courts.

Here’s how to start:

Create your core documents (POAs, will, trust if needed)

Review beneficiary forms on pensions, ISAs, and life insurance

Talk to your loved ones and appointees—clarity avoids conflict

Set a calendar reminder to review your plan every 2–3 years or after major life changes

"Estate planning isn’t about fearing death. It’s about living with confidence and clarity—knowing your family is covered, no matter what happens."

Estate Planning Is a Gift You Leave While You’re Still Here

You don’t need to be ultra-wealthy to have an estate plan—you just need people you care about and things worth protecting.

Yes, it takes time and perhaps a bit of legal cost.

But the alternative is far more expensive—in time, money and heartache.

Take control now. Write the script for how your life—and your legacy—will be managed. Because if you don’t, someone else will.

Risk Warning: This is for informational purposes and does not constitute financial advice, which should be based on your individual circumstances. Full disclaimer below.

The Thinking Skill That Could Save You Thousands

The Mental Model No One Taught You (But Should Have)

“All I want to know is where I'm going to die, so I’ll never go there.”

— Charlie Munger

That quote might sound morbid at first. But it hides a powerful truth—a timeless thinking strategy that’s been quietly used by some of the world’s most successful investors.

It’s called inversion.

And if you apply it consistently, it could save you not just money—but regret, stress and costly misjudgements.

What If the Best Way to Win Is to Simply Avoid Losing?

We often believe investing success is about being smarter, faster or luckier. Finding the next 10x fund. Timing the market perfectly. Riding the wave before it crashes.

But here’s the reality: most investors don’t fail because they lack brilliance.

They fail because they overlook risks.

That’s where inversion comes in. Instead of asking, “How can I succeed?”, inversion asks:

“How could this fail?”

“What could go wrong?”

“What mistake am I about to make without realising it?”

By identifying how things can go wrong before you act, you sidestep the mistakes that wipe out gains, confidence and progress.

Real-World Examples of Inversion at Work

1. Buying a share of a company?

Instead of asking, “What will make this go up?”, ask,

“What would have to go wrong for this investment to fail?”

Maybe the business is deeply in debt.

Maybe it’s a cyclical stock and you’re buying at peak optimism.

Inversion helps you spot hidden risks, before they cost you.

2. Chasing a hot mutual fund?

Ask,

“What would make this fund underperform or disappoint me?”

Maybe the fund manager just changed.

Maybe recent returns are driven by short-term sector trends.

Maybe it’s too large to remain nimble.

3. Feeling FOMO?

When a stock surges 40% in a week, it’s tempting to jump in.

Inversion flips the script:

“What needs to be true for me to lose money chasing this hype?”

Often, the answer is: it’s overpriced, you don’t understand it and you’re driven by emotion—not logic.

Inversion Helps You Avoid the Mistakes That Really Matter

Here’s a short list of how investors often lose money—not by bad luck, but by ignoring common-sense risks:

Taking on leverage without understanding it

Ignoring valuations

Following the herd

Investing emotionally

Failing to maintain an emergency fund

Mistaking noise for signal

Buying in euphoria, selling in panic

Avoid just a few of these traps, and you’ll already be ahead of most.

Inversion isn’t pessimistic. It’s protective.

It helps you play defence in a game where survival is underrated.

Because the longer you stay in the game, the more compounding can quietly work in your favour.

Use Inversion Before Your Next Financial Move

Here’s a practical framework to use right away:

Before you invest in anything—ask yourself:

What could go wrong with this?

What assumptions am I making that might not be true?

Have I seen others make this mistake before—and how?

Would I still invest if this stock didn’t have recent momentum?

If this fails, what would I regret not noticing?

This isn’t about fear. It’s about clarity.

You’re not stopping yourself—you’re strengthening yourself.

Avoiding Stupidity Compounds Better Than Chasing Genius

If I could sum up everything I’ve learned, it would be this:

Success doesn’t come from brilliance. It comes from avoiding stupidity, consistently.

And stupidity often wears the mask of confidence.

Inversion helps you see behind the mask.

Next time you’re excited about an opportunity, or afraid of missing out, pause. Ask:

What am I not seeing?

How could this go wrong?

What would a cautious version of me do here?

And then—act with clarity, not just conviction.

Because in a world chasing the right answer, the real edge lies in avoiding the obvious mistake.

That’s inversion.

And that’s the kind of thinking that lasts.

Risk Warning: This is for informational purposes and does not constitute financial advice, which should be based on your individual circumstances. Full disclaimer below.📞 Contact us today to review your wealth strategy and see how prepared you are for the long haul!

Top Trending News In Finance

Here are the 3 most important financial news, you need to know about!

#➌ Fed and BoE holds rates steady, eyes two cuts in 2025, with the first post-Liberation Day SEP showing weaker growth, higher inflation and rising unemployment. The outlook disappointed, adding to market unease.

#➋ US Senate passes landmark GENIUS stablecoin bill, setting first federal rules for digital dollars and signalling crypto’s rising influence. Meanwhile, Visa and Mastercard shed over $75 billion of market cap this week.

#➊ Trump confirms US strikes on Iran’s nuclear sites, hitting Fordow, Natanz and Esfahan in a major escalation alongside Israel. The move ends US mediation efforts and risks wider conflict.

Thanks for staying connected and being part of the Fast Financier’s Inner Circle! I look forward to sharing more insights with you next time. Until then, keep striving toward your goals and remember—Feel free to hit reply if you need any guidance or have questions. You can also chat with us on WhatsApp here 💬. Wishing you continued success on your financial journey!

Kind regards,

Gavin Pannu

Tradenomic Financial

0203 376 0575

gavin@tradenomic.co.uk

LinkedIn | Website | Book Discovery Call

An important Risk Warning:

Your home may be repossessed if you do not keep up repayments on your mortgage. Levels and bases of, and reliefs from taxation are subject to change and their value will depend upon personal circumstances. Taxation and pension legislation may change in the future. Tax treatment is based on individual's unique circumstances. The Financial Conduct Authority (FCA) does not regulate Wills, Inheritance Tax Planning or Trust advice.

The performance of your investments is subject to risk(s). Its performance may fluctuate based on movements in the market and economic condition(s). Capital at risk. Currency movements may also affect the value of investments. The value of an investment may fall as well as rise. You may get back less than you originally invested. Past performance is not a reliable indicator of the future performance.

Tradenomic Financial is the trading name of Tradenomic Limited which is an Appointed Representative of Julian Harris Financial Consultants, authorised and regulated by the Financial Conduct Authority No. 994930.

As a regulated professional, I aim to be straightforward and provide tools to help you on your journey to financial freedom. Please note, all content shared here is for educational purposes only and not to be seen as specific financial advice. I don’t know your unique circumstances, so general insights may not apply to you. The views expressed are my own.

While we use reliable sources and take care in compiling information, all data and opinions are subject to change without notice. This content is not a recommendation or solicitation to buy or sell securities. Investments carry risk, so please conduct your own research and consult an authorised adviser. This newsletter and any correspondence email is for informational purposes and does not constitute financial advice, which should be based on your individual circumstances. The content within contains our observations of current trends and does not constitute a personal recommendation.

Additional Resources:

🔗 Curious about your financial standing? Use our Net Worth Calculator to find out where you stand today!

🔗 Visualise the trends! Explore our Financial Markets Chart Gallery to stay ahead of the curve.

🔗 Check your credit score now and gain valuable insights to help you stay on top of your financial health. Try it FREE for 30 days, then £14.99 a month - cancel online any time.

Life’s Big Questions to Ask Yourself: